https://spore-share.com or sporeshare.blogspot.com

It is very important to equip and educate ourselves with the Trading or investing knowledge.

Don’t rely on tips! Ensure we have a proper plan in place whenever we enter a trade.

Don’t speculate and trade without knowing what you are trying to achieve.

Only trade when the trading opportunity arise.

All information provided is just just for sharing.

(Trade/Invest base on your own decision!)

Frasers Cpt Tr - She is trading at 2.20, yield is about 5.47 percent of which I think is quite a good yield level! Gearing below 40% for this rare local retail mall reit counter! Pls dyodd.

Today, after Attending SATS AGM went over to Tanjong Pagar and bought some atas pie to try! Looks delicious!

Their top 2 seller is Nutella, Wild cheese and Yuzu. Bought them and try.

FCT (Frasers Cpt Tr) - Nibbled a bit at 2.17 after locked in profit for KDC! At 2.17 yield is about 5.55 percent seem quite a good yield!

Frasers Cpt Tr - She is trading at 2.12, yield is about 5.69 percent, which is a good yield level!

Gearing below 40 percent, NAV 2.26. Looks like boat is back! A good pivot point would be at 2.10 level! Pls dyodd.

FCT (Frasers Cpt Tr) - Nibbled a bit at 2.17 after locked in profit for KDC! At 2.17 yield is about 5.55 percent seem quite a good yield!

She has nicely retreated from 3.35 to close at 3.14, looks rather interesting!

I think the uptrend mode is still intact!

A great pivot point would be at 3.11 to 3.12 for a bounce-off to rise up to test 3.40 and above.

Pls dyodd.

19th July 2024 :

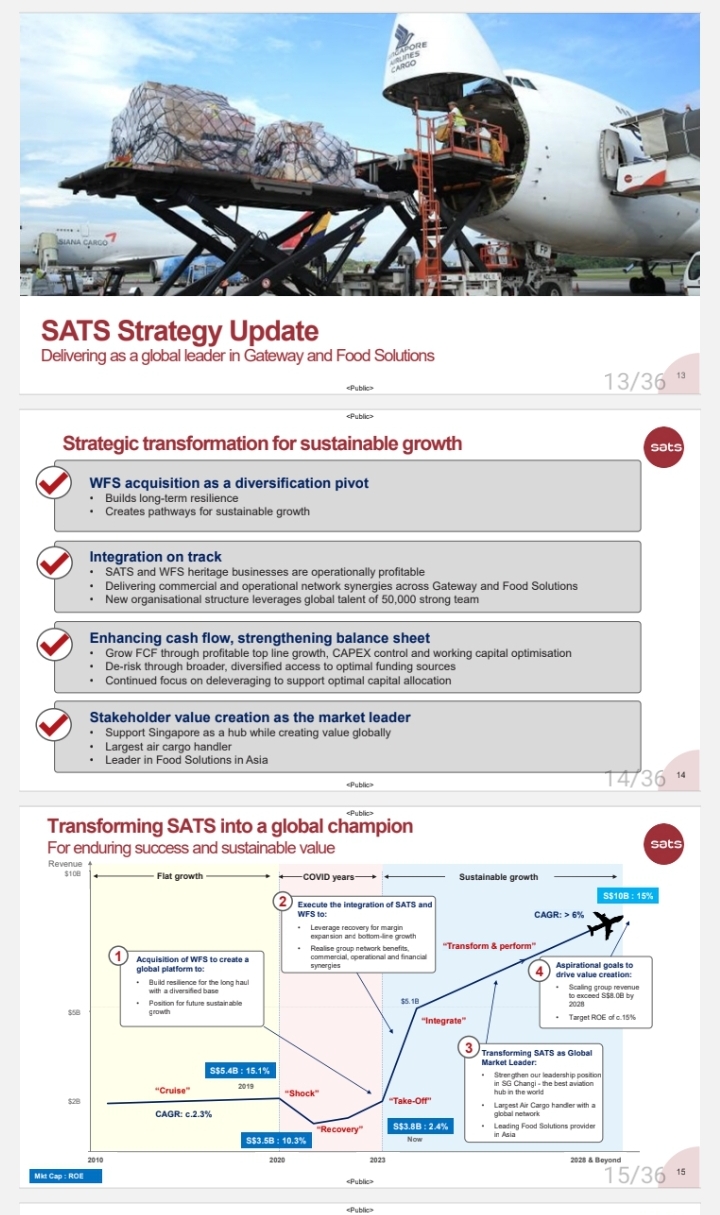

SATS AGM - 11am today(19th July 2024) at Grand Copthorne Waterfront, dont forget!

No food provided, lousy! The mgmt is not thoughtful! Give us twist voucher $15. Many voices out to them SATS doing food businesses yet didn't serve shareholders with food during AGM, very embarrassing!I Think Next year they may include.

Ceo said they are looking at the 1+1 integration to get a 3 instead of 2. Top 20% customers can provide potential enormous growth. WFS achieve productivity of saving costs of about 2-3%. Generate cash flow of 260m in 4q 2023 this may help to reduce the repayment of loan. Assets light, mainly on leases. Generating healthy cash flows for both Food and WFS.

Debt to equity 1.63x versus 0.5x previously. Want to know their difficulties in achieving RoE 15%.1 year integration (Food and gateways )is not easy. Getting to know the ppl beside acquiring the infrastructure. Cherish their staff to grow with the company. He is flexible to receive call in the wee hours. They are committed to achieve ROE of at least 15% or higher. Very strong teams globally.

SATS - She had run up to hit my target price of 3.32, awesome! I had taken this opportunity to secure the profit at 3.34 yesterday! Beautiful!

SATS- A Very nice Long greenish candlestick appearing on the chart yesterday and closed well at 3.29 , up 17 cents coupled with quite a high volume this is rather bullish!

Likely to test 3.32 than 3.40 and 3.60 . Pls dyodd.

SATS - She has a Nice breakout at 3.02, trading at 3.11 likely to continue to trend higher towards 3.32 level.

Pls dyodd.

SATS - She is rising up to revisit 3.00 soon!

A nice breakout smoothly will likely see her testing 3.22 and above! Pls dyodd.

SATS - She has again managed to reclaimed 2.90 and is now trading at 2.93, looks like the uptrend direction will continue! Fantastic!

SATS - AGM is on 19th July 11am at Grand Copthorne Waterfront Hotel level 4, do take note!

May be got nice kopi plus snacks!

SATS- She has retreated from 2.99 to touch 2.86, looks rather interesting! Likely to continue to trend higher!

Pls dyodd.

Gapped up this morning, fantastic!

Likely to rise up to test 2.94 again!

Pls dyodd.

SATS - FY results is out! Declared Final dividend of 1.5 cents, Awesome! Gross Revenue is up three-fold to 5.1b.

XD 24th July. Pay date 8th August.

Net profit of 56.4m reversing from last year net loss of 26.5m. Finally, they are back to profitable, Fantastic!

Strong balance sheet and healthy cash flow, solid!

Quote: SATS is on an ambitious plan to increase revenue by about 60 per cent to $8 billion over the next four years, as it works to build on its sterling set of full-year results that exceeded expectations.

“We have a clear strategy for each of the group’s business lines, and we have a strong operating platform from which to do it.”

These are growing revenue to underpin sustained business growth; driving operating leverage through better cost efficiency and productivity; rationalising its portfolio; repaying debt while optimising cash flow; as well as returning value to shareholders.

Mr Mok summarised this as Sats’ 3Rs: repay loans, re-invest in capital expenditure and resume dividends. On that last point, the group declared a final dividend of 1.5 cents per share for the full year to March 31.

Wilmar Intl - The price is fluctuating between 3.07 to 3.23 looks like we may see a breakout or breaking down scenario!

The director has been supporting in buying back the share may be they know something better than us! Pls dyodd.

First Half results will be out on 13th August. Interim dividend of 6 cents is coming!

Wilmar Intl - Looks like she is going down to test 3.07 than 3.00!

Pls dyodd.

Wilmar Intl - Chart wise, bearish mode! The director keeps buying back share but the share price keep drifting lower! I think testing 3.07 than 2.98 soon!

Pls dyodd.

Wilmar Intl - FY 2023 results is out! 2nd Half net profit is down 27.1 percent to 989.3m versus 1264.3m last year! FY net profit is down 35.3 percent to 1566m versus 2419m.

Final dividend of 11 cents declared same as last year, i think the results is not bad!

XD 29th April.

Pls dyodd.

TA wise, bearish mode!

High probability she may go down test 3.26 than 3.23 with extension to 3.0p.

Pls dyodd.

Results is due on 21st February.

Chart wise, bearish mode!

She may likely go down to test 2.98/3.00.

Breaking down of 3.00 plus high volume she may go further down to revisit 2.80 Than 2.43.

Pls dyodd.

Wilmar Intl - She has broken down 3.38 level seem rather Negative and may likely go down to test 3.00! Do take note!

Pls dyodd.

This piece of news reported on the media not sure will it affects the share price! Please dyodd.

Quote : A Chinese subsidiary of Asian food giant Wilmar International F34 0.29% has denied allegations by a city prosecution agency that one of its units was partially accountable for a trade fraud that led to a 5.2 billion yuan (US$725 million) loss for a state-owned company.

Wilmar Intl - She is drifting lower, looks rather interesting! Likely to go down to test 3.39 again! Do take note!

Yearly dividend of 17 cents, yield is 4.94% at 3.44 of which i think is quite a gd yield level!

Breaking down of 3.38 we may see sliding down toward 3.00.

Pls dyodd.

Wah, crucial moment!

I think is good to monitor and wait for market confirmation!

Yearly dividend is 17 cents. Yield is 4.73%. NAV 4.22.

Pls dyodd.

TA wise, bearish mode!

If 3.60 cannot hold the high chance she will go down to test 3.53/3.50. Breaking down of 3.50 plus high volume we may likely see her going down to test 3.28 than 3.00 and 2.94.

Pls dyodd.

Wilmar Intl - Results is out Net profit is down 52.7% to 550m, Total Revenue is down 10% to 32538m.

Declared same interim dividend of 6 cents.

Lower contribution from Food and Feed and I industrial products despite higher sales volume.

Free cash flow of 1.89b.

I think the results is not bad!

Let's see how she fares next week!

Please dyodd.

Wilmar International Limited, founded in 1991 and headquartered in Singapore, is today Asia’s leading agribusiness group. Wilmar is ranked amongst the largest listed companies by market capitalisation on the Singapore Exchange.

Supported by a multinational workforce of about 100,000 people, Wilmar embraces sustainability in its global operations, supply chain and communities.

An Expanding Global Footprint:

From its humble beginnings, Wilmar has today become a global leader in processing and merchandising of edible oils, oilseed crushing, sugar merchandising, milling and refining, production of oleochemicals, specialty fats, palm biodiesel, flour milling, rice milling and consumer pack oils:

Largest edible oils refiner, specialty fats and oleochemicals manufacturer as well as leading oilseed crusher, producer of consumer pack oils, flour and rice and one of the largest flour and rice millers in China

One of the largest oil palm plantation owners and the largest palm oil refiner and palm kernel and copra crusher, specialty fats, oleochemicals and biodiesel manufacturer in Indonesia and Malaysia

Largest producer of branded consumer pack oils in Indonesia

Largest branded consumer pack oils, specialty fats and oleochemicals producer and edible oils refiner as well as leading oilseed crusher, sugar miller, refiner and ethanol producer in India

One of the largest investors in oil palm plantations, one of the largest edible oils refiners and producers of consumer pack oils, soaps and detergents as well as third largest sugar producer in Africa

Largest raw sugar producer and refiner, a leading merchandiser of consumer brands in sugar and sweetener market and largest manufacturer of bread, spreads and sauces in Australia

Leading refiner of tropical oils in Europe.

First quarter 2023 Financial No. update :

The Group reported net profit of US$391.4 million and core net profit of US$381.9 million for the quarter, with stronger sales volume recorded in both Food Products and Feed & Industrial Products segments. Excluding the gain on dilution of interest in Adani Wilmar Limited of US$175.6 million recognised in 1Q2022, the Group reported a growth in net profit of 10.3%, while core net profit grew by 16.5% during the quarter.

Despite the challenging operating conditions, the Group managed to deliver a satisfactory set of results for 1Q2023. Higher volume of sales was achieved across all businesses. Sugar milling and merchandising did well with higher sugar prices. Oilseed crushing did better due to higher volume and good coverage of raw materials. Food Products segment saw an overall increase in volume of sales, largely due to higher medium pack and bulk products sales, particularly in China. Plantation profit was reasonable even though palm oil prices came down significantly from the peak. Shipping performed well but palm oil refining margin was poor.

Cash Flow & Balance Sheet The stable performance for the quarter led the Group to generate higher operating cash flows before working capital changes of US$756.1 million. With the decline in commodity prices and seasonal reduction in overall inventory balance during the quarter, working capital requirements for the Group decreased accordingly, leading to lower net debt of US$17.27 billion as of 31 March 2023 (31 December 2022: US$18.75 billion). Consequently, net gearing ratio for the Group improved to 0.84x as of March 2023 (FY2022: 0.94x). This led to the Group generating strong cash inflow from operating activities of US$2.17 billion in 1Q2023. At the end of the reporting period, the Group had unutilised banking facilities amounting to US$26.32 billion.

Outlook Results for the quarter ended 31 March 2023 were satisfactory, despite the uncertain macro-economic outlook at the start of the year. With our diversified and integrated business strategies, we are cautiously optimistic that performance for the rest of the year will remain satisfactory.

The company paid out Final dividend of 11 cents + interim dividend of 6 cents, total 17 cents for FY 2022. The current share price is $3.97, yield is about 4.28% of which I think is quite a decent yield!

Chart wise, bearish mode!

She may likely continue to trend lower!

Short term wise, I think likely to go down to test 3.90.

Breaking down of 3.90 plus high volume that may likely see her falling down further towards 3.75 then 3.46 level.

CapitaLand Ascendas REIT - She had managed to bounce off from 2.56 and closed well at 2.72, coupled with high volume looks rather bullish and may likely continue to trend higher towards 2.85 and 2.97-3.00!

Huat ah!

Pls dyodd.

CapitaLand Ascendas REIT - Did you managed to catch it at 2.57 few days ago?

Today she is trading at 2.74, a nice rebound! Likely to rise further up towards 2.83 and above! Pls dyodd.

CapitaLand Ascendas REIT - Great price is here, dont miss out! At 2.57, yield is quite nice at about 5.8 percent for this Giant industrial cum Data Centres reit, under famous manager, gearing below 40 percents plus index counter, I think golden opportunity to take a look at the current pivot price level!

Results will be out on 30 July 2024, dividend is coming!

Next Fed meeting is on 30 to 31 July.

Pls dyodd.

CapitaLand Ascendas REIT - Wah, Great sales is here! At 2.63, yield is about 5.67 percent for this blue chips index reit counter of which I think is looking rather interesting!

If 2.60 cannot hold then we may see her going down to revisit 2.47 that will provide me an opportunity to add!

Pls dyodd.

CapitaLand Ascendas REIT - I think gd reit is on sales! Yielding 5.5 percent, a blue chips index reit is offering us a great opportunity to take a closer look at the current price of 2.70! Pls dyodd.

CapitaLand Ascendas REIT - I think GSS price is back! At 2.66, yield is about 5.6 percent for this industrial cum Data Centres reit plus a sti index component stocks and a giant, great opportunity to take a look! Dont miss out!

Pls dyodd.

CapitaLand Ascendas REIT - I think Great price snd GSS sales is here! Trading at 2.71, yield is about 5.5 percent of which I think is quite a good yield level! When interest rate started to come down she will not be trading at this kind of yield level! Pls dyodd.

CapitaLand Ascendas REIT - 2nd Half results os out! Gross Revenue is up 11% to 761m, NPI is up 4.6 percent to 641m, Distribution Income is down 1.9 percent to 326.9m. DPU is down 6.1 percent to 7.441 cents.