Chart wise, looks pretty interesting!

It has managed to bounce-off from the low of 77 cents and rises higher to hit 85.5 cents.

Will we be seeing a follow-through action !

Short term wise, I think it may likely re-attempt 85.5 cents.

Crossing over with ease + good volume that may drive the price higher towards 90 cents then 95 cents with extension to 1.00.

Not a call to buy or sell.

Pls dyodd.

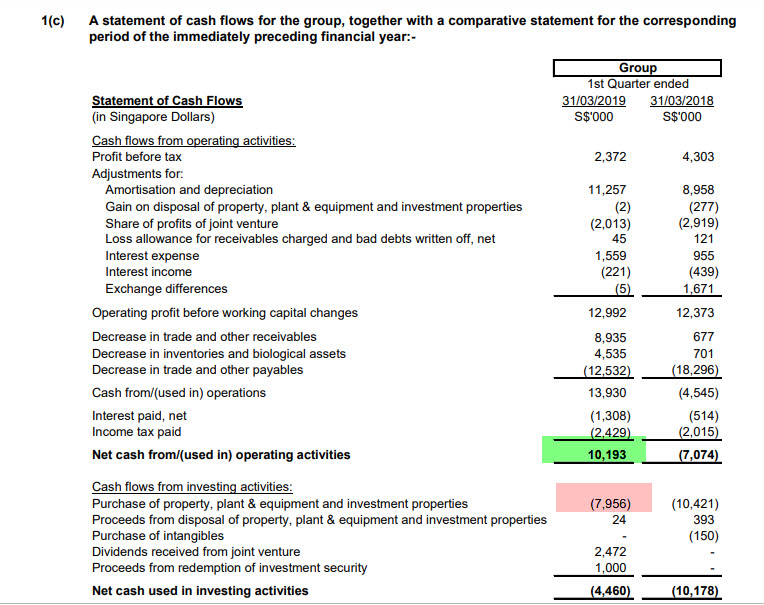

1st Quarter 2019 result - The Group posted a revenue of approximately $27.2 million for this period as compared to $17.7 million in the

previous corresponding period. The increase was mainly due to the recognition of revenue from the sales of its

development properties in Singapore and higher rental income from its investment properties including YOTEL

Singapore Orchard Road (“YOTEL”).

Hence, the Group posted a profit of approximately $5.1 million as compared to $0.6 million in the previous

corresponding period.

The Group’s profit attributable to Owners of the Company was approximately $5.5 million as compared to $1.5 million

in the previous corresponding period.

The right-of-use asset was mainly related to lease of the office units occupied by the Group in Hong Kong.

The increase in other investments was mainly due to purchase of shares and bonds and valuation of its other

investments at fair value as at 31 March 2019.

The non-current asset held for sale in 2018 was disposed off in February 2019.

The lease liabilities as at 31 March 2019 were due to the adoption of SFRS(I) 16 with effect from 1 January 2019.

The Group increased its non-current loans and borrowings due to drawdown of its secured loans to redeem its $120

million 4.75% unsecured fixed rate notes on its due date, 22 March 2019 and for its purchase of other investments.

Subsequently, on 28 March 2019, the Company issued $100 million 4.2% unsecured fixed rate notes from its $600

million Multicurrency Debt Issuance Programme to partially repay these secured loans.

The decrease in loans and borrowings under current liabilities was mainly due to the redemption of its $120 million

unsecured fixed rate notes on its due date.

The decrease in trade and other payables was mainly due to the payments of accrued development costs, employee

benefit expenses and finance expense.

The increase in current tax liabilities was mainly due to provision of tax for this period.

The total debts to equity ratios is pretty healthy at 0.25 .

The current price of 84 cents is trading at P/B of 0.304x.

NAV is 2.76.

Management has been buying back share from 79,79.5 to 82.5 cents .

https://links.sgx.com/FileOpen/_FORM1_CSE_Final.ashx?App=Announcement&FileID=562653

https://links.sgx.com/FileOpen/_FORM1_CSE_Final.ashx?App=Announcement&FileID=562653